S&P500 LDN Open Trading Update 19/5/26

S&P500 LDN Open Trading Update 19/5/26

***QUOTING ES1! FOR CASH US500 EQUIVALENT LEVELS, SUBTRACT POINT DIFFERENCE***

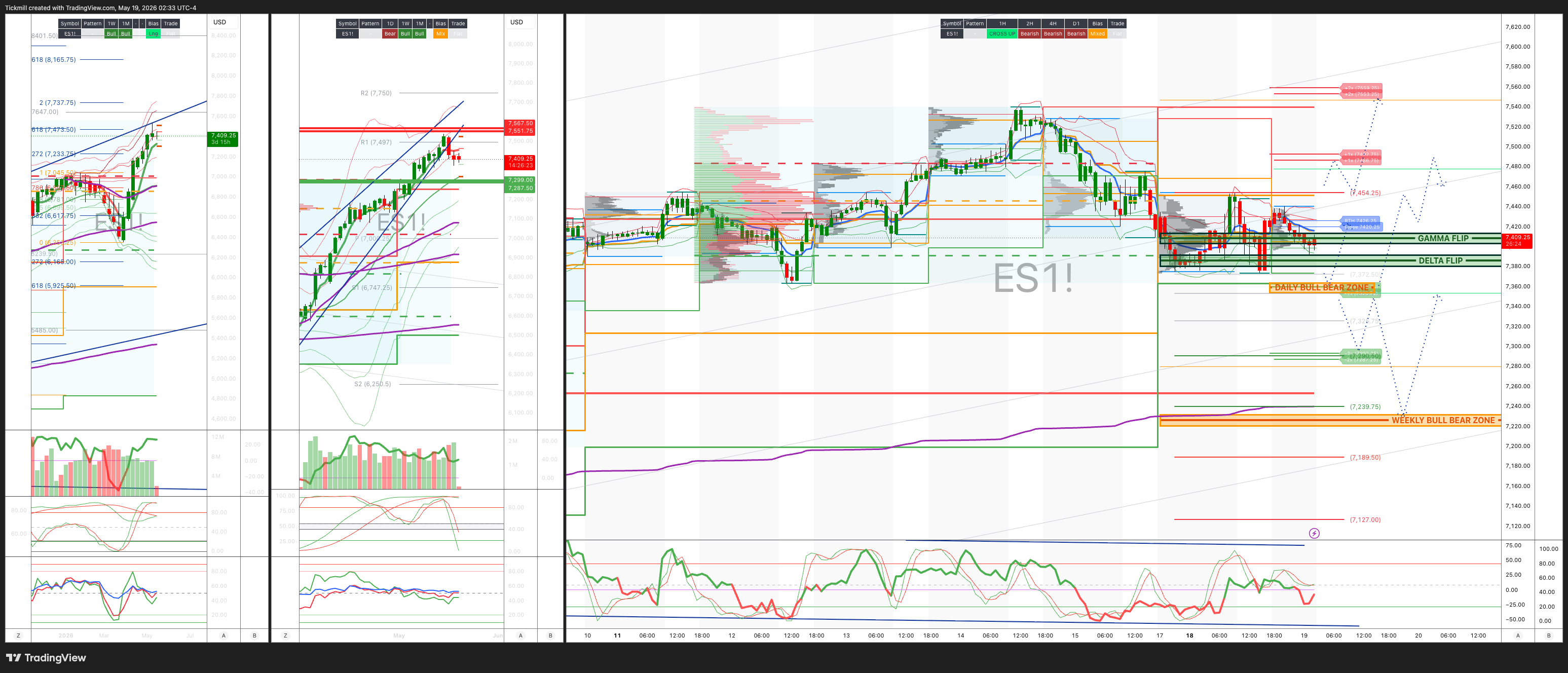

WEEKLY BULL BEAR ZONE 7220/30

WEEKLY RANGE RES 7286 SUP 7550

June MOPEX Straddle: 274pt range implies a OPEX to OPEX range of [7134, 7683]

June QOPEX Straddle is 546.4pt giving us a range of [5960,7052]

JHEQX Q2 Collar 6189/6290 - 6865/6955

DEC2025 OPEX to DEC2026 OPEX is 945 points giving us a range of [5889,7779]

SPX PUT/CALL RATIO 1.07 (The numbers reflect options traded during the current session. A put-call ratio below 0.7 is generally considered bullish, and a put-call ratio above 1.0 is generally considered bearish)

DAILY VWAP BEARISH 7455

WEEKLY VWAP BULLISH 7292

MONTHLY VWAP BULLISH 6898

DAILY STRUCTURE – OTFL - 7454

WEEKLY STRUCTURE – OTFH - 7363

MONTHLY STRUCTURE - OTFH - 6514

Balance: This refers to a market condition where prices move within a defined range, reflecting uncertainty as participants await further market-generated information. Our approach to balance includes favouring fade trades at the range extremes (highs/lows) while preparing for potential breakout scenarios if the balance shifts.

One-Time Framing Higher (OTFH): This represents a market trend where each successive bar forms a higher low, signalling a strong and consistent upward movement.

One-Time Framing LOWER (OTFL): This describes a market trend where each successive bar forms a lower high, indicating a pronounced and steady downward movement.

DAILY BULL BEAR ZONE 7350/60

GAMMA FLIP 7409

DELTA FLIP 7386

DAILY RANGE RES 7492 SUP 7359

2 SIGMA RES 7559 SUP 7293

VIX BULL BEAR ZONE 19

TRADES & TARGETS

LONG ON REJECT/RECLAIM DAILY BULL BEAR ZONE TARGET RTH/CLOSE

***ADDITIONAL SETUPS & TARGETS HIGHLIGHTED ON THE CHARTS***

(I FADE TESTS OF 2 SIGMA LEVELS ESPECIALLY INTO THE FINAL HOUR OF THE NY CASH SESSION AS 90% OF THE TIME WHEN TESTED THE MARKET WILL CLOSE ABOVE OR BELOW THESE LEVELS)

GOLDMAN SACHS TRADING DESK VIEW - ‘Muted’

US equities finished close to flat at the index level, but the tape was much more unstable beneath the surface. The S&P 500 slipped 7bps to 7,403, the NDX fell 45bps to 28,994, the Russell 2000 lost 65bps to 2,775, while the Dow managed to gain 32bps to 49,686. Volumes were elevated at 20.7bn shares versus a YTD daily average of 19bn, and the close saw a modest USD 750mn MOC imbalance to sell. Cross-asset price action was still dominated by the energy shock: WTI rose another 81bps to USD 106.27, front-month Brent is now around USD 112/bbl, the US 10-year was unchanged at 4.60%, gold gained 44bps to USD 4,561, DXY fell 28bps to 99.01, Bitcoin lost 164bps to USD 76,972, and VIX fell 331bps to 17.82.

The market’s message was not in the headline index move. It was in the factor tape. This was another session of aggressive momentum unwind, with prior losers and high-beta momentum shorts leading while the 12-month winners and high-beta momentum longs sold off sharply. The GS TMT Momentum pair is now down roughly 14% from its peak in just three sessions, nearly matching the late-March pullback and approaching the kind of drawdowns seen during prior stress episodes. The AI Beneficiaries versus AI-at-Risk basket posted its worst session ever, falling 6.69%, which makes clear that this is not random churn but a direct unwind of crowded AI and momentum positioning.

The fact that the S&P was nearly unchanged while the AI/momentum complex suffered a large drawdown is important. Index risk looks contained, but factor risk is high. This is the kind of environment where portfolios can lose money even if the benchmark barely moves, especially if they are concentrated in the same AI, TMT, high-beta, and 12-month winner trades that have dominated recent performance. The outperformance of equal-weight S&P also reinforces the rotation dynamic: leadership is broadening away from the most crowded mega-cap and AI beneficiaries, at least tactically.

Macro remains a constraint. The Strait stayed largely closed over the weekend, oil drifted higher, and there was no incremental progress on US/Iran. Even with the 10-year unchanged on the day, 4.60% is still a difficult level for long-duration growth assets, especially when oil is above USD 100 and Brent is above USD 110. The equity market can tolerate higher yields when earnings momentum is strong, but the combination of high oil, sticky inflation risk, and stretched AI positioning makes it much less forgiving. The energy shock is not yet breaking the index, but it is clearly raising the hurdle for crowded growth trades.

Activity was quiet despite elevated market volume. The floor was only a 3 out of 10 and finished 3% for sale versus a 30-day average of 176bps better to buy. Single-stock activity was muted, with the street largely frozen ahead of major catalysts later in the week. That makes sense: investors have little reason to press large new risk until they see NVDA earnings, Google I/O, WMT, and additional consumer discretionary prints. The market is caught between a macro overhang and a heavy micro calendar, which can keep index action muted even while factor rotations are violent.

The derivatives tape also showed a controlled but nervous market. Vol flows were generally quiet, and spot down/vol down persisted, which suggests there was no broad panic bid for index protection. But skew was bid across the curve, showing that investors still want downside convexity into event risk. The rest-of-week straddle went out around 1.42%, which reflects the importance of this week’s catalysts. VIX expiry is also tomorrow, not Wednesday, due to next month’s Juneteenth holiday, which may matter for short-term vol mechanics.

The most important near-term event is NVDA. After a 14% drawdown in the GS TMT Momentum pair in three sessions, the AI complex is entering earnings with much cleaner but still fragile positioning. A strong NVDA print could quickly stabilize the group and restart the AI leadership trade, especially if management confirms durable data-center demand, margin resilience, supply visibility, and hyperscaler capex momentum. But if NVDA merely meets high expectations, or if investors focus on memory constraints, gross margin pressure, China exposure, or a slower forward cadence, the unwind can continue.

Google I/O is the other major AI catalyst. The market will look for evidence that AI software and platform monetization are broadening beyond infrastructure spend. Investors want to see product progress, developer traction, agentic AI use cases, cloud demand, and any signs that AI is improving search or enterprise monetization rather than simply raising capex. A strong Google event could help rotate AI enthusiasm from semis toward software/platform beneficiaries. A disappointing one would reinforce the idea that the AI trade has become too concentrated in capex hardware winners.

WMT matters for a different reason. The consumer has been the weak link in the market, and high gasoline prices add pressure to lower-income spending. WMT will be the cleanest read on trade-down, grocery inflation, discretionary weakness, margin management, and whether the consumer squeeze is worsening or stabilizing. If WMT is solid, it could support a broader rotation into laggards and equal-weight exposure. If it disappoints, it would strengthen the bearish consumer narrative and make the market even more dependent on AI.

The trading takeaway is that this is no longer a clean “buy the AI dip” tape. The long-term AI thesis may still be intact, but the short-term positioning unwind is real and has not yet clearly exhausted itself. With oil still rising, yields elevated, and major catalysts ahead, investors should avoid adding aggressively to the most crowded AI and momentum longs before confirmation from NVDA and Google. For now, it makes more sense to reduce factor concentration, keep hedges in place, and use equal-weight or revision-supported laggards as a way to stay exposed to equities without relying entirely on crowded mega-cap AI leadership.

At the same time, the absence of broad index stress argues against turning outright bearish. VIX fell, the S&P barely moved, and equal-weight outperformed. This looks more like a violent internal rotation than a market-wide de-risking event. The best stance is tactical and disciplined: respect the momentum unwind, avoid crowded longs into event risk, keep oil/rates hedges on, and be ready to re-engage quality AI only if the upcoming catalysts validate the earnings and capex story.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% and 73% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

Patrick has been involved in the financial markets for well over a decade as a self-educated professional trader and money manager. Flitting between the roles of market commentator, analyst and mentor, Patrick has improved the technical skills and psychological stance of literally hundreds of traders – coaching them to become savvy market operators!