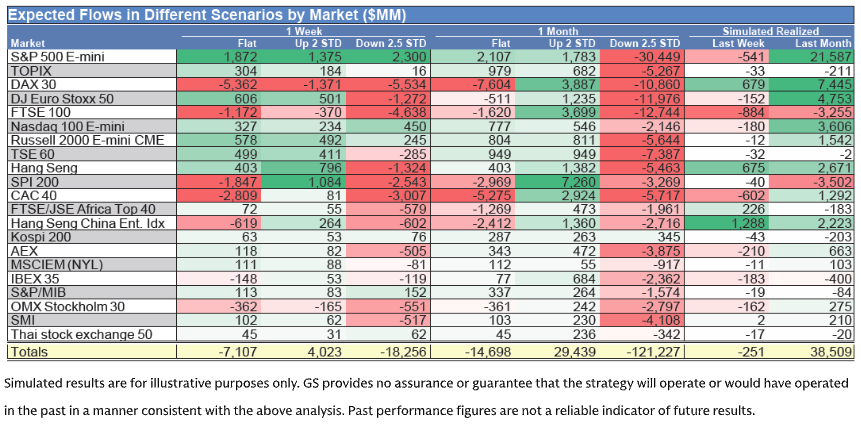

Institutional Insights: Goldman Sachs SP500 Flows & Positioning Update 19/5/26

Buybacks, Risk Appetite, and the Narrow-Highs Problem

Corporate buyback activity remains an important support for the tape. The buybacks desk saw flows finish last week at 1.2x 2025 YTD ADTV and 1.4x 2024 YTD ADTV, with activity skewed toward Financials, Consumer Discretionary, and Health Care. Open-market buyback momentum is now in full swing as companies exit the Q1 earnings blackout window, giving corporates more flexibility to deploy discretionary capital.

That matters because, in a market dealing with AI momentum unwinds, higher oil, and elevated yields, corporate demand can provide a stabilizing bid. But it does not eliminate the bigger issue: the S&P 500 is making repeated new highs while breadth is deteriorating and risk appetite is extremely elevated.

Buyback window is now supportive

The post-earnings period is typically one of the strongest windows for open-market repurchases. Companies have completed earnings, legal restrictions are lower, and management teams have maximum discretion over timing and execution.

That is showing up in the desk’s flow data. More than one-third of current order count is now made up of discretionary orders, meaning companies are actively choosing to deploy capital rather than simply running automated programs.

This is a constructive technical support for equities, especially on dips.

The strongest buyback activity is concentrated in:

Financials

Consumer Discretionary

Health Care

That sector skew is notable because it is not purely an AI/mega-cap tech bid. It may help support market broadening if momentum continues rotating away from crowded AI leadership.

Buybacks can cushion, but not necessarily lead

The important nuance is that buybacks are supportive, but they rarely solve valuation, breadth, or macro problems on their own. Corporate demand can reduce downside volatility and create dip-buying support, particularly in single names where repurchases are large relative to liquidity.

But if the market is facing a large factor unwind or yield shock, buybacks usually cushion rather than prevent drawdowns.

In the current setup, buybacks are a meaningful offset to:

AI momentum unwind

Elevated oil prices

Higher long-end yields

Weakening breadth

Investor hesitation ahead of catalysts

But they are not a reason to ignore the extreme level of risk appetite.

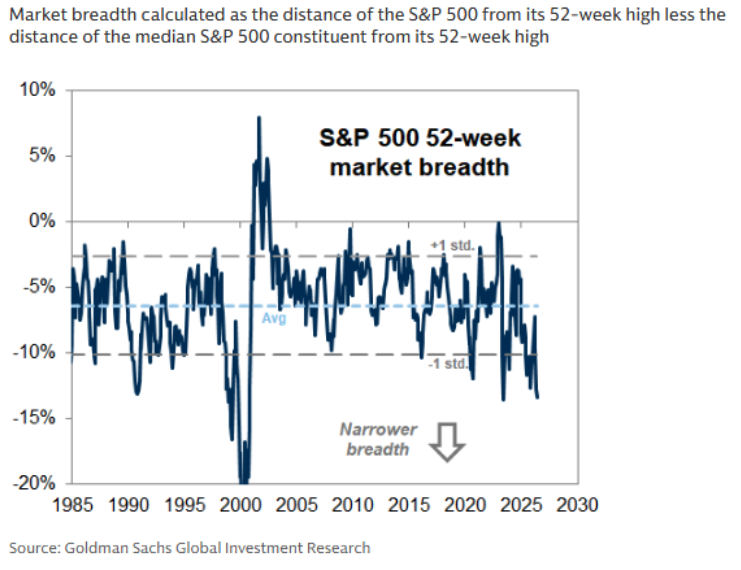

New highs with declining breadth

The S&P 500 has registered 14 new highs over the past month, but this has occurred alongside declining market breadth.

That is the classic narrow-leadership problem. The index continues to rise because large-cap winners are doing the heavy lifting, while more stocks are failing to participate. This can persist for a while, especially if mega-cap earnings remain strong, but it creates fragility.

Narrow highs mean:

The index looks better than the median stock.

Leadership is increasingly concentrated.

Portfolios benchmarked to the index may feel forced into crowded winners.

Momentum becomes more important than fundamentals.

Any reversal in leadership can hit the index disproportionately.

This is why the recent AI/momentum unwind matters. If the market is making highs on narrow leadership, the leading cohort cannot stumble too much without creating broader index risk.

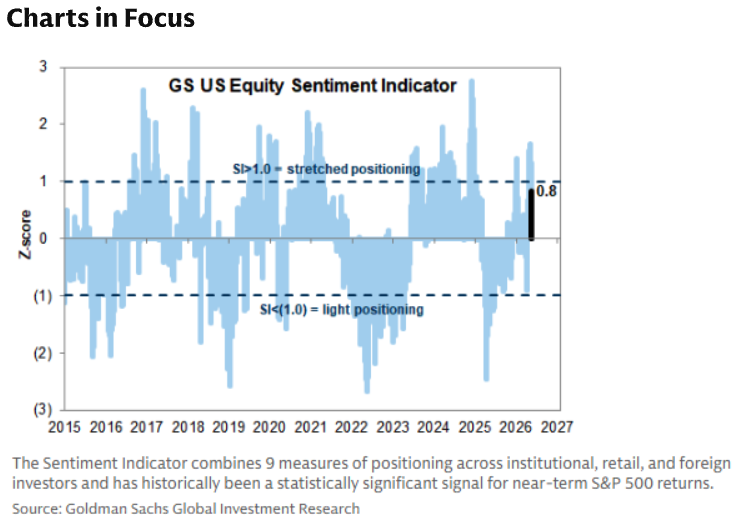

Risk Appetite Indicator at extreme levels

Goldman’s Risk Appetite Indicator breached 1.1 last week, surpassing levels seen at the start of the year and reaching the highest reading since 2021. That places it in the 99th percentile since 1991.

This is a clear sign that investors are embracing risk aggressively. It does not automatically mean equities must fall immediately, but it does mean forward returns are likely to become less asymmetric on the upside.

Historically, comparable episodes since the 1960s have shown:

More limited upside for broad equities

Some correction risk

Larger and more symmetric tails for Momentum

Greater vulnerability to factor reversals

In plain English: when risk appetite is this high, the easy money has usually already been made.

Momentum tails are larger and more symmetric

The most important factor implication is for Momentum. At elevated risk appetite levels, Momentum does not simply offer strong upside continuation. It tends to develop larger two-sided tails.

That means the same factor that has been driving performance can become a source of volatility. Momentum can still rally sharply if catalysts validate the story, but it can also unwind violently if positioning is crowded or macro conditions tighten.

That fits the current tape. The AI/momentum complex has already seen a sharp drawdown, while prior losers and equal-weight exposure have started to outperform. This is exactly the kind of rotation risk that tends to appear when risk appetite is stretched.

Macro backdrop still prevents a fully bearish stance

Despite elevated risk appetite and weak breadth, the macro backdrop is not uniformly bearish. Growth remains resilient, earnings revisions are still positive, and AI productivity optimism remains a powerful long-term support.

The report’s key nuance is that risk appetite is elevated, but the macro backdrop remains benign enough to support equity returns as bullish sentiment lingers.

That means this is not a clear “sell everything” signal. It is more of a “reduce complacency and manage factor concentration” signal.

Supportive macro/equity factors include:

Strong Q1 earnings season

Positive EPS revision breadth across sectors

Corporate buyback demand

AI capex and productivity optimism

Resilient nominal growth

Still-active dip buying

Offsetting risks include:

Oil above USD 100

Long-end yields around restrictive levels

Narrow market breadth

Crowded AI positioning

Elevated risk appetite

Momentum reversal risk

Trading takeaway

The trading message is to respect the corporate bid but avoid chasing narrow highs blindly.

Buybacks should provide downside support, particularly in names and sectors with active discretionary repurchase programs. The post-earnings open window is real, and the fact that flows are running above prior-year ADTV levels is constructive.

But the combination of 14 S&P highs in a month, declining breadth, and RAI in the 99th percentile argues for better risk control. This is a market where broad index upside may be more limited, while factor volatility rises.

The best expression is not outright bearishness. It is more selective equity exposure:

Stay long high-quality companies with positive EPS revisions.

Use buyback-supported names as a source of downside cushion.

Reduce exposure to the most crowded momentum winners.

Add some low-Momentum stocks with positive revisions as rotation hedges.

Consider equal-weight upside where market broadening is possible.

Keep downside protection given elevated skew and geopolitical/oil risk.

Avoid assuming new index highs mean healthy participation.

Corporate buybacks are now a meaningful support as companies exit earnings blackout, with flows running 1.2x 2025 YTD ADTV and 1.4x 2024 YTD ADTV. That should help cushion dips, especially in Financials, Consumer Discretionary, and Health Care.

But the broader technical setup is more fragile than the index suggests. The S&P 500 has made 14 new highs in a month even as breadth has declined, while Goldman’s Risk Appetite Indicator has reached the 99th percentile and the highest level since 2021.

The conclusion is balanced: buybacks and resilient macro conditions can keep the market supported, but upside is less clean and momentum reversal risk is elevated. This is a market to stay invested in, but with less factor concentration, more attention to breadth, and stronger hedging discipline.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% and 73% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

Patrick has been involved in the financial markets for well over a decade as a self-educated professional trader and money manager. Flitting between the roles of market commentator, analyst and mentor, Patrick has improved the technical skills and psychological stance of literally hundreds of traders – coaching them to become savvy market operators!